Exposing the Realities of Market Manipulation

Based on Value?

In the ever-shifting landscape of investment markets, appearances can be deceiving. At first glance, investment markets present themselves as a straightforward interplay of supply and demand, guided by rational decisions and clear financial data. However, a closer examination reveals a more complex and sometimes opaque world, where not everything is as it seems.

This cryptic nature stems from a variety of factors: the influence of unseen market forces, the unexpected impact of global events, and the often-underestimated role of human emotion in financial decision-making. Additionally, the presence of market manipulation, both subtle and overt, adds another layer of complexity, casting a shadow of uncertainty over what might appear as transparent market movements.

In such an environment, investors navigate a sea of information, where discerning the genuine from the misleading requires not just financial acumen but also a keen understanding of the broader economic, political, and social currents that shape market behavior. The investment markets, therefore, are not just a reflection of numbers and charts, but a dynamic ecosystem influenced by a multitude of often unseen and unpredictable factors.

The industries that have had the biggest growth in share prices are the banking sector, the energy sector (which includes those icky fossil fuels), and the lithium sector (which includes one of the dirtiest kinds of energy in the planet). State Street Funds, Vanguard, and BlackRock have control over all of them.

These "funds" frequently induce bubbles in the markets for their customers.

Not for the general public. Not for the impoverished, and definitely not for the middle class. They increase the affluent's riches.

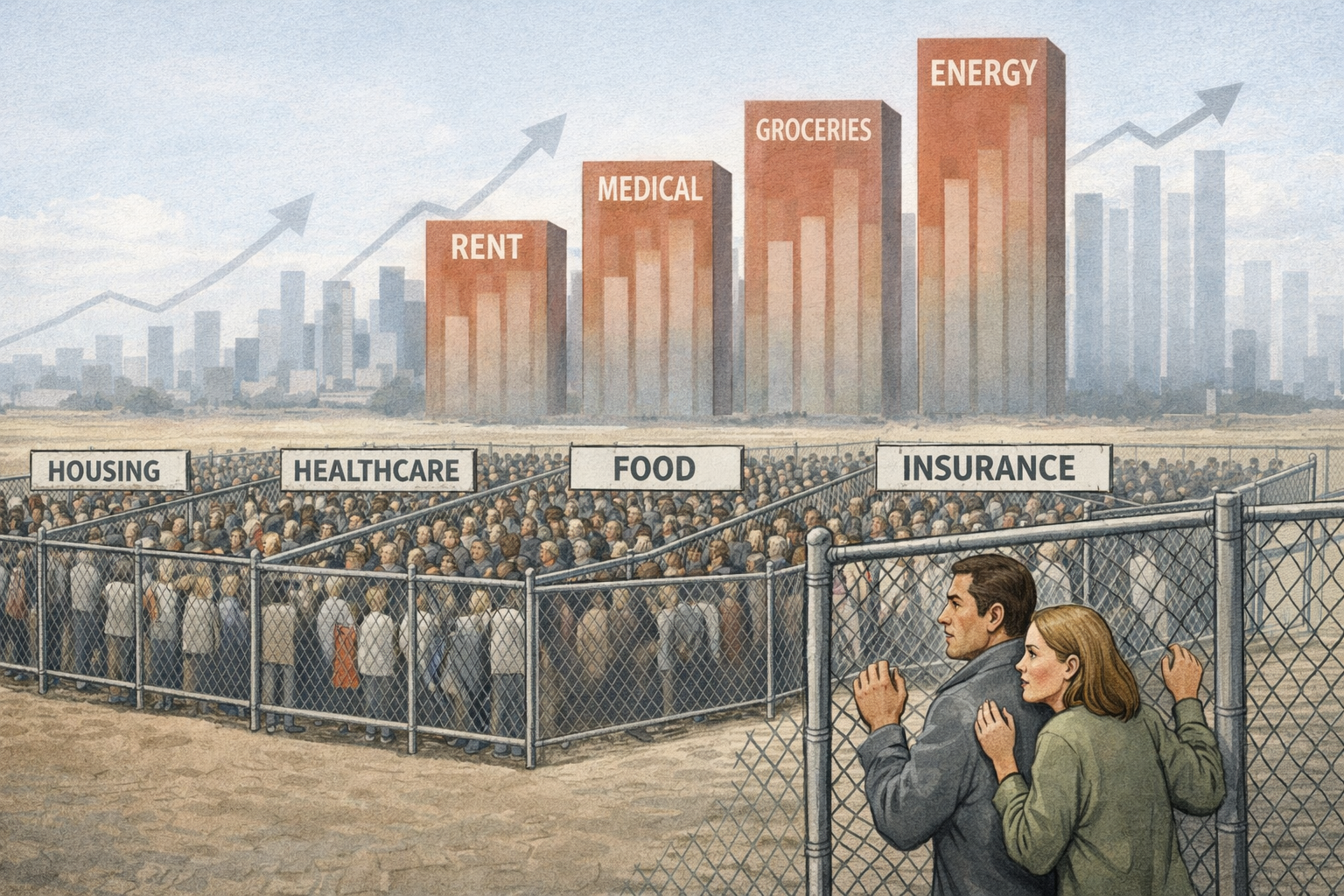

The inflation rate is clearly a ridiculous mixture that was created in a witch's brew.

The 3.4% that the Social Security division is allowed to use to calculate increases in 2024 ignores all fundamental services and instead depends on the "personal consumption expenditures" of the urban population. Requirements for the "basket of goods" include computers, prescription drugs, mortgage payments, and college tuition. Indeed, in a real way, mortgage payments, including those for 2% fixed-rate mortgages purchased in 2019. They leave out food and energy because they "fluctuate too much."

Has The Fed Wrecked The Dream of Home Ownership?

This from a recent Wall Street Journal article:

Homeownership has become a pipe dream for more Americans, even those who could afford to buy just a few years ago, it is now less affordable to buy a home, and the math isn’t changing any time soon. That means buyers get a lot less home for their dollar. Before the Fed started raising rates, a person with a monthly housing budget of $2,000 could have bought a home valued at more than $400,000. Today, that same buyer would need to find a home valued at $295,000 or less.

Prospective home buyers are facing a double whammy in the economy, as cheap mortgage debt has sent property prices skyrocketing. That is to say, because there are artificially fewer homes available for sale, housing prices are rising rather than decreasing when interest rates rise in accordance with standard economic principles. Thus, if you take the higher mortgage rate and double it by the even higher property price.

In my reading of "How the Fed Wrecked the Dream of Homeownership," David Stockman confirmed that the Federal Reserve's policy of keeping interest rates low has significantly contributed to inflated home prices and the unaffordability of home ownership in the U.S. Despite appearances, the problem isn't high mortgage rates, which are historically low, but rather the exorbitant cost of homes driven by cheap mortgage debt and limited housing availability.

Over the past fifty years, home prices have dramatically outpaced wage growth and the Consumer Price Index, creating a severe housing affordability crisis. This situation is exacerbated by the Fed's post-2000 policies, which, instead of boosting new housing investments, have inflated the prices of existing homes, making homeownership a distant dream for many.

The Second Largest Contributor of Private Debt

An article in Armstrong Economics highlights the story that auto loan debt in the U.S. has now surpassed student loan debt, reaching $1.582 trillion. This escalation is largely due to the rising costs of vehicles, compelling consumers to take larger loans. The transition towards electric vehicles and inventory shortages have exacerbated this issue. Moreover, government policies pushing for an increase in EVs and the associated higher costs are placing a significant financial burden on consumers.

Auto financing has become more restrictive as lenders react to this trend. Amidst these developments, there's a debate similar to student loan forgiveness: whether auto debt, particularly for more expensive EVs, should be forgiven. This raises questions about the fairness and sustainability of such financial policies.

The Roaring 20s

The parallels between the "Roaring Twenties" and today's markets and economy are being widely discussed. The 1920s were a time of significant technological, social, and economic change, characterized by a booming stock market, wealth accumulation, and cultural and artistic innovation.

"Value investors have to be patient and disciplined, but what I really think is you need not to be greedy. If you're greedy and you leverage, you blow up." - Shelby M.C. Davis